A fresh round of pressure is weighing on the global smartphone market as memory shortages continue to disrupt production and pricing. In the first quarter, worldwide shipments reached only 289.7 million units, according to IDC, marking a 4.1% decline from the same period a year earlier.

The slowdown is not only about softer demand. IDC points to the memory crisis as a major factor behind the weaker performance, since tighter component supply has slowed distribution and pushed manufacturing costs higher across the industry.

Premium brands still hold the line

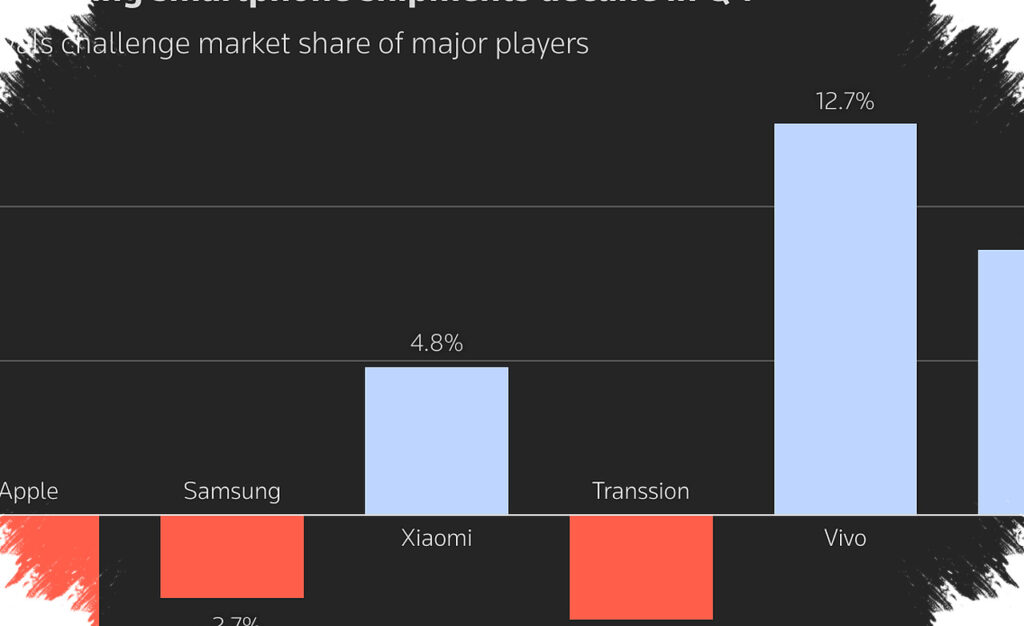

Even in a weaker market, the top of the ranking has changed little. Samsung remained the world’s largest smartphone vendor, with shipments estimated at 62.8 million units and a market share of 21.7%.

IDC said demand for the Galaxy S26 Ultra helped support Samsung’s performance, while the Galaxy A57 and Galaxy A37 were also important in keeping sales momentum in place. That combination allowed Samsung to stay ahead despite broader pressure on the market.

Apple followed closely in second place with 61.1 million units and a 19.6% share. IDC noted that the iPhone 17 series continued to attract buyers, especially in China, which helped Apple post positive growth even as many other major brands faced larger setbacks.

The narrow gap between Samsung and Apple also highlights one clear trend in the current market: premium devices remain more resilient than lower-priced models when component costs rise. Buyers in higher-value segments appear less sensitive to price pressure, especially in markets with stronger purchasing power.

Lower-end phones face the sharpest squeeze

The situation looks much tougher for entry-level devices. IDC said consumers in the sub-USD 200 category are likely to see fewer choices because rising memory prices are forcing manufacturers to delay launches or raise retail prices.

Anthony Scarsella, Research Director for Mobile Phones at IDC, said the 4.1% decline in the first quarter is only the beginning of a more difficult stretch. He noted that mature markets such as the United States are still relatively stable because premium models, trade-in incentives, and financing options continue to support demand.

That resilience does not extend evenly across the rest of the market. As memory costs rise and other component expenses also move higher, manufacturers have less room to keep low-margin products competitive, which makes portfolio planning more complicated.

The rest of the top five

Behind the two leaders, Xiaomi stayed in third place with 33.8 million shipments, although that figure was about 8 million units lower than in the first quarter of 2025. Oppo ranked fourth with 30.7 million units and a 10% market share, while Vivo placed fifth after shipping 21.2 million devices for a 7.5% share of the global market.

The composition of the top five shows how concentrated the smartphone business remains around a handful of major names. At the same time, IDC’s figures suggest that only a small group of vendors is currently able to grow while component pressure continues to rise.

Here is the ranking of the five largest vendors according to IDC:

- Samsung — 62.8 million units, 21.7% share

- Apple — 61.1 million units, 19.6% share

- Xiaomi — 33.8 million units

- Oppo — 30.7 million units, 10% share

- Vivo — 21.2 million units, 7.5% share

IDC also expects average selling prices, or ASP, to rise as the memory crisis continues. The research firm said memory prices are not likely to stabilize until the second half of 2027, leaving the smartphone industry exposed to ongoing tension between component supply, device prices, and consumer purchasing power.