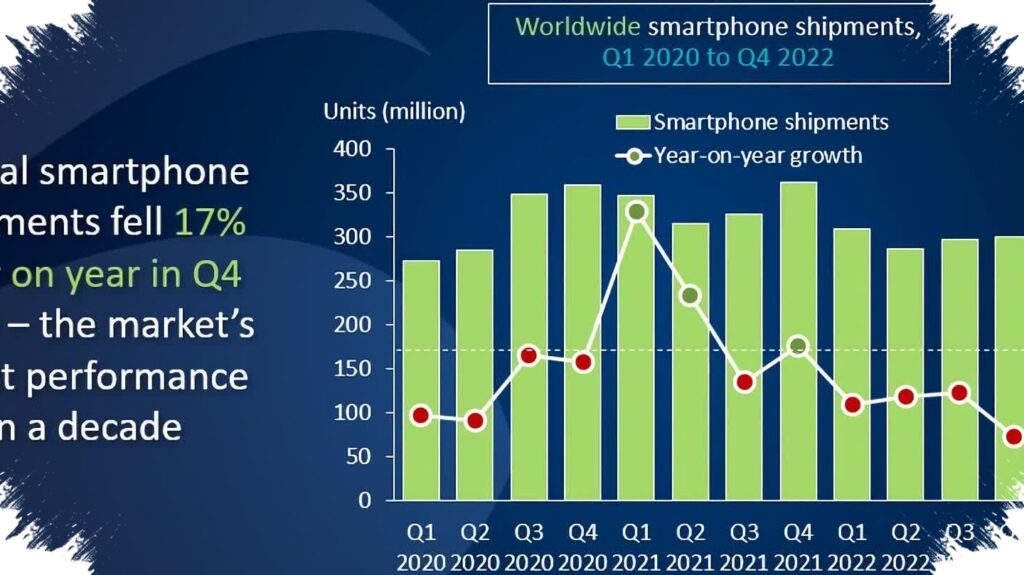

India’s smartphone market lost momentum sharply in the first quarter, with shipments down 3 percent year on year, according to Counterpoint Research’s Monthly India Smartphone Tracker. That made it the weakest first-quarter performance for the market in six years.

The decline comes as handset makers face a difficult mix of higher component costs, repeated retail price adjustments across segments, and still-muted consumer demand. Even with major brands continuing to push new launches, the market has slowed rather than recovered.

Rising costs are reshaping pricing

Counterpoint said the ongoing surge in memory prices continued to lift supply-chain costs, while currency swings added more pressure on vendors. As a result, many manufacturers were forced to reconsider pricing strategies in order to protect margins.

Those changes are already visible in retail pricing. More than 80 smartphone models saw an average price increase of 15 percent in the first quarter, according to the report. That adjustment, however, did not produce a rebound in shipment volumes.

About one-third of smartphone launches were advanced into the first quarter as brands tried to respond to component-cost pressure, but enthusiasm from buyers remained weak. Counterpoint expects price hikes of 15 to 20 percent may still continue in the next quarter, driven by the same cost conditions.

Brands still competing for share

Even in a softer market, some major brands continued to hold strong positions. Vivo led smartphone shipments in India with a 21 percent share, supported by a larger number of launches, solid demand in the premium mid-range through its latest V series, and disciplined channel execution.

Samsung took second place, helped by promotions across the Galaxy A07, Galaxy A36, and Galaxy A56 lines, along with strong early demand for the Galaxy S26 series, especially the Galaxy S26 Ultra. Counterpoint said Samsung’s broad portfolio across price bands also helped stabilize performance, with the biggest shipment contribution coming from the Rs. 15,000 to Rs. 20,000 segment.

Oppo remained in third place with a 14 percent share. Its sales were supported by the A and K series in the budget category and the Reno lineup, and it was the fastest-growing brand among the top five with 8 percent year-on-year growth.

Competition deepens across segments

Xiaomi and its Poco sub-brand stayed relevant in the mid-range and affordable tiers. Xiaomi held 7.9 percent share, while Poco reached 4.8 percent, both supported by double-digit growth in the Rs. 10,000 to Rs. 20,000 bracket.

Realme ranked fifth with an 11 percent share, driven largely by online strength and demand for the Realme P3 Lite and Narzo 80 Lite. Apple held 9 percent share, supported by continuing demand for the iPhone 17 series.

Among the fastest growers overall, Nothing, including CMF, stood out with 47 percent year-on-year growth. Counterpoint linked that rise to a more aggressive offline push, the opening of its first exclusive retail store in India, and market response to the Phone 4a series. In the premium segment above Rs. 45,000, Google was the fastest-growing brand, rising 39 percent.

Chipset leadership and the outlook ahead

On the chipset side, MediaTek led total shipments with a 49 percent share. Qualcomm remained dominant in the premium Android segment with more than 50 percent share, underscoring its continued strength at the higher end of the market.

Tarun Pathak, Research Director at Counterpoint Research, said the industry is likely to stay under pressure in the near term. He warned that the next quarter could post a double-digit decline because memory prices remain elevated and weak demand in the entry-level segment continues to weigh on volumes.

For the full year, Counterpoint expects India’s smartphone market to fall 10 percent year on year. Pathak also pointed to persistent component inflation, especially memory, which he said has increased fourfold over the last three quarters, keeping purchasing power under strain and lengthening replacement cycles.

Source: www.gadgets360.com