Apple’s latest market move reflects more than a short-term reaction to a strong product cycle. Shares climbed by nearly 4 percent as investors responded to demand for the iPhone 17 and MacBook Neo, while the company’s outlook and financial results helped reinforce confidence in its growth path.

The rally came even though iPhone sales in the latest quarter came in slightly below expectations. That miss did not overshadow Apple’s broader performance, especially after the company lifted its forecast for next quarter sales growth to 14-17 percent, well above the market’s expectation of around 9.5 percent.

iPhone 17 demand keeps investor focus on growth

The iPhone 17 remained at the center of investor attention as demand for the device helped shape optimism around Apple’s stock. Tim Cook said demand was very strong, but supply chain flexibility was not enough to fully meet component needs.

That supply constraint meant the latest iPhone sales figures did not fully reflect consumer interest. Even so, the strength of demand suggested Apple still has room to convert product momentum into future revenue if production constraints ease.

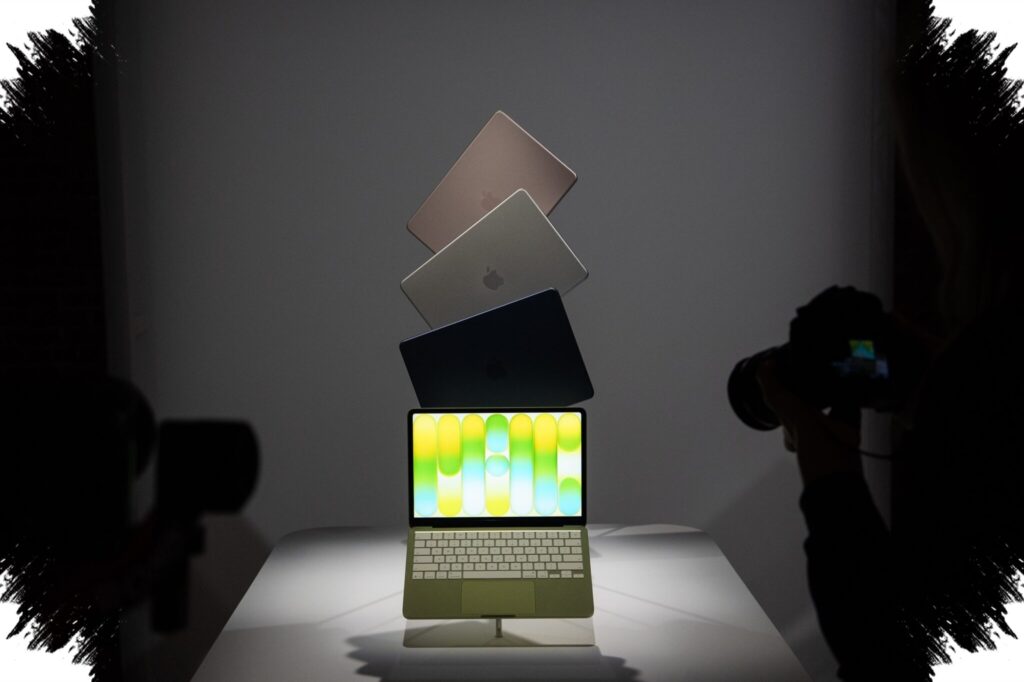

MacBook Neo adds a new growth angle

MacBook Neo also emerged as an important contributor to Apple’s recent results. The more affordable laptop helped Mac revenue beat market expectations, with sales reaching $8.4 billion.

Its significance goes beyond a single quarter. The product may help Apple reach a lower-priced laptop segment that has long been dominated by Chromebooks, expanding the company’s reach into a market it has not aggressively pursued before.

Revenue, earnings, and margins stay firm

Apple reported revenue of $111.18 billion and earnings of $2.01 per share, both ahead of analyst estimates. Those numbers pointed to a business that remained resilient despite supply limitations and pressure across parts of the hardware cycle.

The company’s profit margin also held at around 49 percent. At the same time, Apple announced a $100 billion share buyback program, a move that typically signals management confidence in valuation and cash generation.

Services and China help balance the picture

Apple’s services business added another layer of support to the quarter. Revenue from that segment, including the App Store, reached $30.98 billion and also topped expectations.

Performance in China came in better than forecast as well. That matters because China remains one of the most closely watched parts of Apple’s growth story amid intensifying competition.

Still, Apple signaled caution about cost pressure ahead. The company warned that component prices, especially memory chips, are expected to rise soon and could weigh on margins in the next quarter.

AI remains the next point of attention

Beyond phones, laptops, and services, investors are now watching Apple’s approach to artificial intelligence. The company is expected to outline more of its AI strategy during its annual developer conference in June.

Apple has not yet spent on AI at the same scale as some of its rivals, but reports say its research and development spending has risen sharply. That keeps the spotlight on whether the company can translate heavier investment into a clearer AI direction while its core businesses continue to support the stock.