AI is moving beyond answering questions and is now beginning to complete transactions on its own. In India, that shift has taken a notable step forward after Pine Labs introduced a system designed to let AI agents shop, place orders, and pay through UPI without human intervention at every stage.

The development matters because payments have long been the main bottleneck for AI agents. They could search for products, compare prices, and make decisions, but they still had to stop when authentication through a UPI MPIN was required.

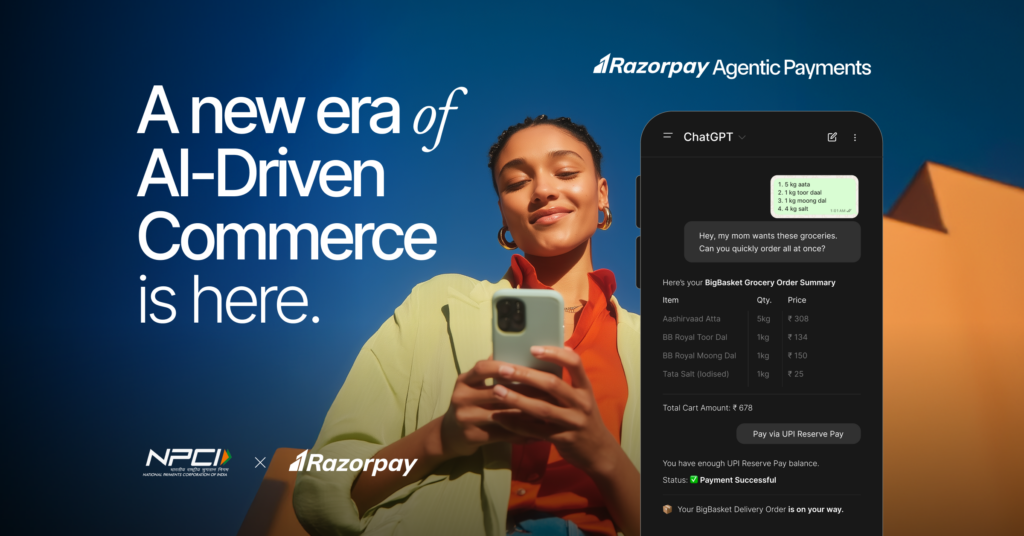

A payment flow built for autonomy

Pine Labs says the system, called Pine Labs Payment Protocol or P3P, is built on existing UPI infrastructure rather than a brand-new payment rail. It uses UPI One Time Mandates and Reserve Pay to let an AI agent continue after a user grants initial authorization.

With that setup, the user does not need to approve each transaction manually. According to Pine Labs, the consumer authorizes the process once at the start, and the AI agent can then browse, choose, negotiate, and pay without repeated interruptions.

UPI One-Time Mandate was originally created so users could approve future payments in advance. It temporarily blocks a fixed amount in the bank account for a later transaction.

Reserve Pay works differently. Powered by NPCI’s Single Block Multiple Debit framework, it is designed for recurring or automatic payments.

In that model, a user first approves a spending limit by entering the UPI PIN. After that, the merchant can debit the exact amount for the service used, such as a monthly subscription.

Pine Labs says combining those two rails is what AI payments have been missing. Instead of building a payment system from scratch, the company is using capabilities that already exist inside the UPI ecosystem.

Controls, limits, and identity checks

The biggest question is security. If AI can spend money, the system must make sure it does not move beyond the limits set by the user.

For that, Pine Labs uses Grantex as a digital identity and authorization layer for AI agents. The system lets the AI prove its identity, receive permission to spend funds, operate within an approved budget, and keep a record of every transaction.

The protocol also uses HTTP 402, which Pine Labs describes as a shared digital language that helps systems request and process payments in a standardized way.

Together, those elements are intended to let AI buy, sell, and make payments on behalf of businesses without requiring human approval for every step. Control remains with the initial authorization, spending limit, and transaction trail.

Already active in a real service

Pine Labs says the system is already running in Gullak. One example shows how AI agents can handle a purchase automatically once the user has set the rules.

A Gullak user can give an instruction such as buying gold worth Rs 500 if the price falls below Rs 16,000 per gram. After the user approves one UPI mandate, the AI agent in the app monitors gold prices automatically and completes the purchase when the condition is met.

In that scenario, the user does not have to approve the payment a second time when the transaction happens. The app only sends a confirmation after the purchase is complete.

This kind of setup shows how AI agents can act on pre-set parameters. The human role shifts from executing the transaction to defining the rules and limits.

What it could mean for online shopping

The same approach could extend to e-commerce. Karan Gupta, Managing Director of Vijay Sales, said P3P could change how customers behave when they usually have to keep checking for discounts.

Instead of repeatedly monitoring the price of a smartphone or refrigerator, a customer could ask an AI agent to buy the product when it reaches a target price. In practice, the AI would work like a personal shopper that keeps watch and does not miss the offer.

For shopping platforms, that could change the trigger point for transactions. Purchases would no longer need to wait for a user to open an app and tap pay, because the decision could be executed automatically within the permitted limits.

The regulatory gap remains

Even if the technology is ready, the rules are not. There is still no RBI framework that specifically defines how AI agents should operate inside India’s UPI payment system.

That gap raises new questions about liability, usage limits, consumer protection, and oversight. UPI One Time Mandates and Reserve Pay were originally created for more specific needs, including IPO applications and recurring subscription payments.

When those mechanisms are used to give AI the power to make autonomous purchases, the risk profile changes as well. For now, the future of the idea will likely depend not only on technical readiness, but also on how quickly payment rules adjust to AI agents.