The global smartphone market slipped back into contraction in the first quarter, as shipments fell 4.1% year over year to 289.7 million units, according to preliminary data from International Data Corporation (IDC). The decline marked the first negative quarter since 2023 and showed that the recent recovery in handset demand has not fully held up against supply and cost pressures.

IDC said the slowdown was driven by an acute memory chip shortage and rising component costs, both of which have pushed up average selling prices and made it harder for vendors to keep devices affordable. The result is a market where premium demand remains resilient, but lower-end segments are feeling increasingly squeezed.

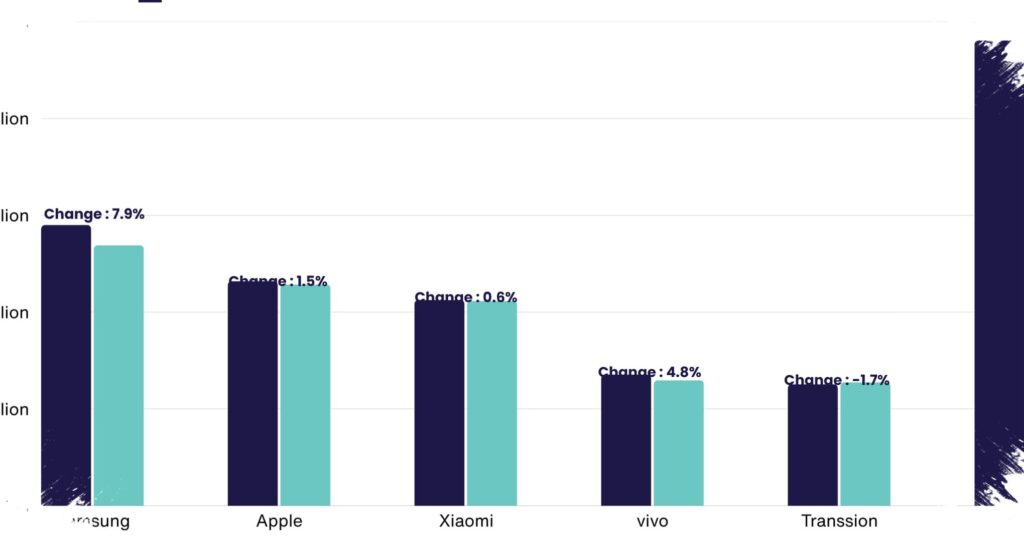

Samsung Holds the Top Spot

Samsung stayed in first place globally with 62.8 million shipments and a 21.7% market share, up 3.6% from a year earlier. IDC linked the performance to strong demand for the Galaxy S26 Ultra and an earlier launch cycle for the Galaxy A36 and Galaxy A57, both of which are expected to support volume for the rest of the year.

Apple followed closely in second place with 61.1 million units and a 19.6% share, rising 3.3% year over year. IDC noted continued interest in the iPhone 17 lineup and said the company posted notable growth in China, a market that has been difficult for many global brands.

The two leaders stood out because they were the only top-five vendors to post annual growth in both shipments and market share. That contrast highlights how the strongest brands are still finding room to expand even as the broader market weakens.

How the Top Five Ranked

- Samsung — 62.8 million units, 21.7% share, up 3.6%

- Apple — 61.1 million units, 19.6% share, up 3.3%

- Xiaomi — 33.8 million units, 11.7% share, down 19.1%

- OPPO — 30.7 million units, 10.6% share, down 9.9%

- vivo — 21.2 million units, 7.3% share, down 6.8%

Outside the top five, other vendors collectively shipped 80.1 million units, down 4.2% from the same period a year earlier. That broader weakness suggests the pressure is not limited to a single region or brand, but is spreading across much of the Android ecosystem.

Lower-Cost Phones Face the Biggest Strain

Xiaomi remained third, but its drop was steep. Shipments fell from 41.8 million units a year earlier to 33.8 million units, showing how quickly demand can soften when pricing pressure rises and value-oriented consumers hesitate.

OPPO took fourth place with 30.7 million shipments, while vivo finished fifth with 21.2 million units. These brands are heavily exposed to mid-range and budget categories, where even small price increases can affect purchase decisions and inventory planning.

IDC said the memory crunch has lifted bill of materials costs, leaving manufacturers with fewer options. Some vendors, including Samsung, have responded with price adjustments on select models, but that strategy can be risky in markets where buyers are highly sensitive to cost.

Premium Demand Still Supports the Market

The data suggests the market is splitting into two very different behaviors. Premium buyers in developed markets, especially the United States, are still willing to upgrade when a product offers clear value or a strong brand pull.

By contrast, growth is harder to sustain in emerging markets, where demand below the $200 price point is especially vulnerable. IDC warned that this category could face even more pressure if memory prices and component costs remain elevated.

That matters because many Android makers rely on high-volume sales from affordable phones to balance their global results. When those models become harder to price competitively, shipment growth can weaken quickly even if flagship devices perform well.

What the Next Few Quarters May Bring

IDC expects volatility to continue in the months ahead as the memory shortage works through the supply chain. The research firm said memory prices may not fully stabilize until the second half of 2027, which means manufacturers will likely keep facing a tough mix of higher costs and cautious consumers.

For now, Samsung’s lead shows that scale, product timing, and premium demand can still outweigh a soft market. But with rivals losing momentum and budget buyers under pressure, the next phase of the smartphone cycle will likely depend on which brands can protect margins without pricing themselves out of the market.