Laptop demand in Indonesia is heading into a more complicated phase as buyers increasingly expect AI-ready features, while manufacturers face tighter component supply and higher production costs. The result is a market where product availability, pricing, and specification choices may shift faster than many consumers expect.

The pressure is coming from two directions at once. On one side, replacement demand is supported by the Copilot+ ecosystem and the end of Windows 10 support, which encourages more users to consider new machines. On the other side, the industry is dealing with a memory crunch and rising input costs that are already reshaping how laptop makers plan their next product cycles.

A market that has not fully recovered

Indonesia’s laptop industry is still trying to regain momentum after the post-pandemic slowdown. In Jakarta’s distribution centers, caution remains visible because the market has not fully closed a decline of nearly 15%, leaving distributors and retailers more selective about inventory.

That restraint matters because sales conditions are no longer driven only by consumer interest. Faster supply, tighter stock control, and the ability to keep prices competitive have become just as important for selling laptops successfully.

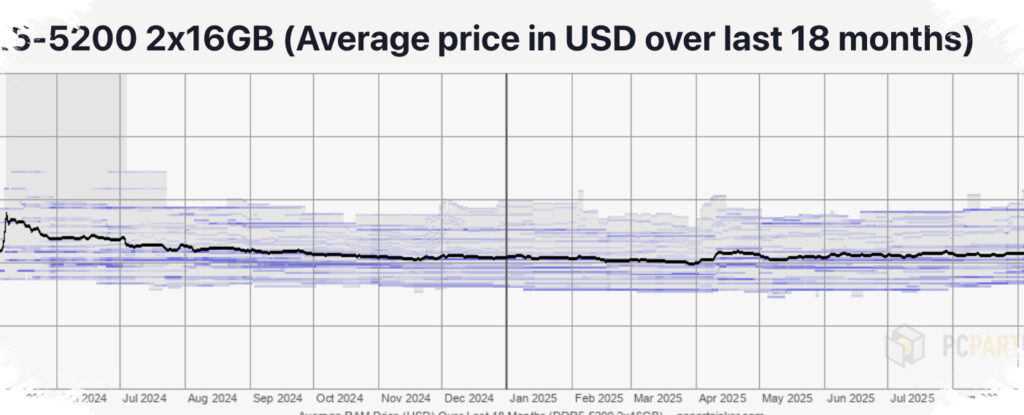

Memory and CPU costs are changing the math

The biggest pressure point is material cost, especially memory and processors. DRAM and NAND, which previously accounted for around 15% of notebook material costs, have risen to more than 30% within a year.

At the same time, Intel has raised CPU prices, with double-digit increases on certain SKUs. When those two major components climb together, a 30–40% increase in laptop prices becomes a realistic scenario for manufacturers and distributors.

In one pricing illustration drawn from the source material, average selling prices could rise by around 40%. A mainstream laptop that previously sat near Rp15 million could move to about Rp21.3 million.

AI features are becoming a purchase requirement

The shift in demand is not a sign of weakness, but of changing expectations. Buyers are paying more attention to thin, light, and all-day portable designs, while AI capability is increasingly viewed as a requirement in the mid-range and premium categories.

Copilot+ and NPU-based functions such as transcription, image processing, and local inference are appearing more often on shopping lists. Yet these features also add cost, because Copilot+ requires at least 16GB of RAM, while many premium designs target 32GB.

That creates a difficult balance for manufacturers. They need to meet the growing demand for AI-ready specifications, but they also have to avoid pricing the product out of reach for consumers in a memory-tight market.

Brand competition remains concentrated at the top

The competitive landscape is still dominated by major players. Lenovo continues to lead the PC and laptop market at roughly 24–25%, while ASUS remains strong in gaming and AI-based PCs.

ASUS ROG is said to hold about 47.6% of the gaming laptop segment. In the AI PC and Copilot+ category, ASUS also sits in the lead with a share approaching 60%, showing how aggressively it has moved toward Microsoft’s early specification standards.

Behind them, Acer, Axioo, Dell, and HP are still pushing for share. Their product refreshes increasingly include NVIDIA RTX 50-series GPUs to keep premium and enthusiast models attractive.

Corporate buyers are becoming more important

The enterprise and government segments are also shaping the market direction. ASUS has been strengthening its offerings for finance, manufacturing, and public-sector customers by emphasizing service, security, and device lifecycle management.

Lenovo and HP remain strong rivals in this space because of their long track records. In many tenders, managed services, Device-as-a-Service, device management, local service networks, and refresh plans aligned with the end of Windows 10 support are key decision points.

Supply constraints may narrow the field further

IDC describes global PC shipment prospects for 2026 as sluggish. Its base-case outlook points to a decline of nearly 5%, while a worse scenario shows a drop of around 9%, even as average PC prices may still rise by 6–8%.

For Indonesia, that environment could favor large brands such as Dell, HP, Lenovo, and ASUS because they have stronger procurement scale and better inventory leverage. Regional brands and white-box assemblers face heavier margin pressure, especially in gaming segments where high RAM has become a standard requirement.

For consumers, laptop choices are likely to narrow into a trade-off between price, upgrade potential, and AI support. The next market move will depend heavily on how quickly DRAM and NAND supply loosens, because that will determine how prices, specifications, and brand power evolve from here.