The global smartphone market entered the first quarter of 2026 under clear strain, with shipments falling 4.1% year on year to 289.7 million units, according to IDC. The decline ended a 10-quarter growth streak that had started in mid-2023 and signals that the industry’s recovery has lost momentum.

The downturn is not being driven by weak interest alone. IDC points to a combination of supply pressure and rising production costs, with the memory shortage emerging as one of the heaviest burdens facing smartphone makers right now.

Rising costs are reshaping pricing

Limited memory supply has pushed manufacturing expenses higher, and those higher costs are being passed through to retail prices in many markets. In some developing countries, smartphone prices are said to have climbed by as much as 40% to 50%, a jump that has quickly cooled demand.

That pressure is especially visible in the entry-level segment, where buyers are the most sensitive to price changes. As phones become more expensive, many consumers are delaying purchases, which in turn reduces shipment volumes for vendors that rely on affordable models.

Vendors respond with defensive moves

Faced with a less predictable supply environment, many manufacturers have adopted a more cautious stance. Some have reduced shipments, cut back marketing activity, or lowered product specifications in an effort to keep costs under control.

This shift has also accelerated premiumization across the market. Rather than chase volume at all costs, several vendors are focusing more heavily on higher-priced devices, where margins are better protected despite ongoing supply-chain instability.

Premium brands remain more resilient

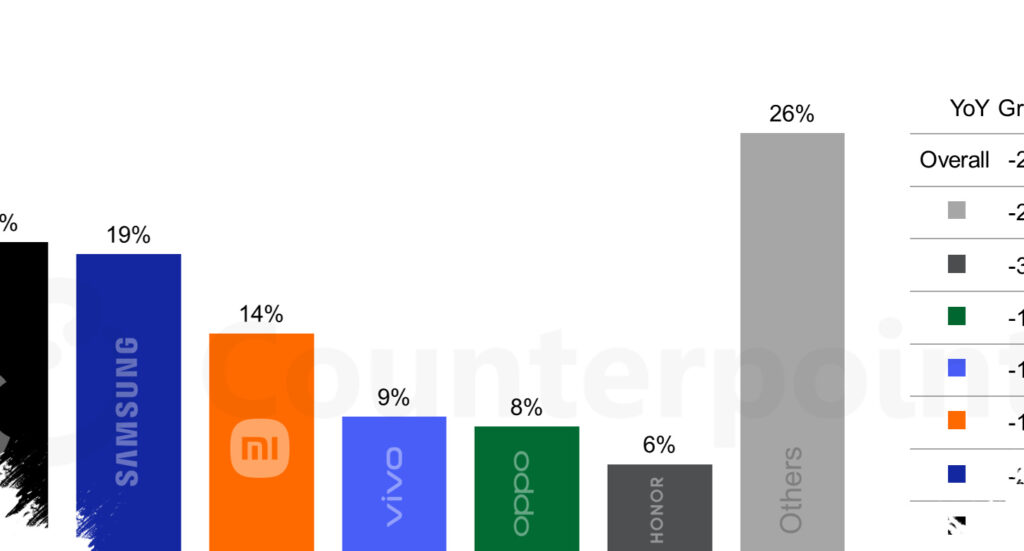

Even as the overall market contracted, Samsung and Apple managed to post positive growth. Samsung held the top spot, supported by strong demand for the Galaxy S26 Ultra and continued strength from the Galaxy A Series.

Apple stayed in second place, helped by the iPhone 17 line, with China playing an important role in its performance. Both companies are seen as better positioned to absorb component stress because of their strong premium focus and established supplier relationships.

Honor posts the sharpest increase

Among the global top 10 vendors, Honor stood out with the fastest shipment growth. IDC reported that Honor’s shipments rose 24% year on year, making it the strongest mover in the group.

That surge was driven by aggressive international expansion that is beginning to pay off. While many rivals were focused on defending their home markets, Honor was able to use the period to widen its reach abroad.

Lenovo, which is sold through Motorola, and Huawei also delivered positive growth. Even so, Honor’s pace was the most notable because it came at a time when the global market was contracting.

Competition among the top five stays tight

Xiaomi remained in third place, although it recorded the largest decline after reducing distribution of older models. OPPO followed in fourth, supported by a strong performance in China, while vivo held fifth place thanks to stable results in its domestic market and India.

The ranking shows that the biggest brands still have room to defend their positions, but the space for expansion is narrowing. Higher component costs and thinner margins are forcing vendors to be more selective about pricing, specifications, and product availability.

IDC expects memory prices to begin stabilizing only in the second half of 2027. Until that pressure eases, the global smartphone market is likely to remain difficult, while faster-moving groups such as Honor may continue to benefit from a more agile expansion strategy.